Introduction

Introduction

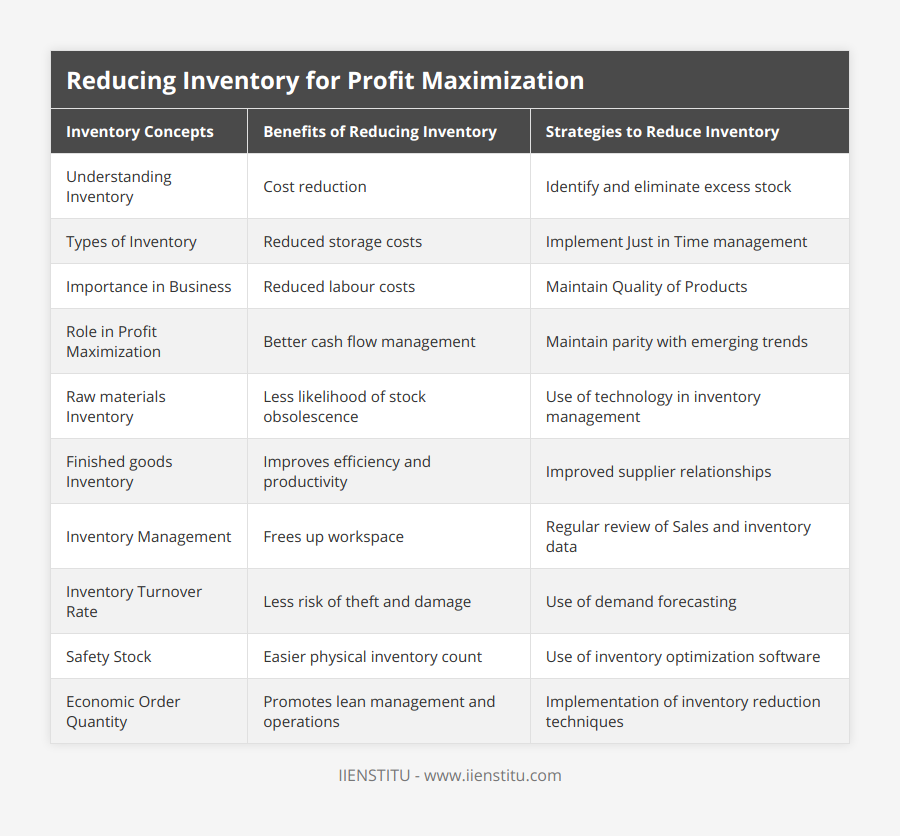

Understanding Inventory

Benefits of Reducing Inventory

Strategies for Reducing Inventory

Conclusion

You know, back when I first started working in my family's small retail business, I vividly remember the overwhelming sight of our cramped stockroom. Boxes piled high to the ceiling, inventory that hadn't seen the light of day in months—maybe even years. We were so focused on stocking up that we didn't realize how much it was costing us. It felt like we were drowning in our own products. It wasn't until we began to understand the true impact of reducing inventory that things started to turn around.

Managing inventory isn't just about keeping enough products on hand; it's about finding that delicate balance between supply and demand. And let me tell you, achieving this balance can make a world of difference in your business's success.

Understanding Inventory

Inventory, in its simplest form, is all the items a company holds that are either ready for sale or will be used to produce goods for sale. Sounds straightforward, right? But there's so much more beneath the surface. Let's dive a bit deeper.

Carload Freight Supply Chain Management Benefits Challenges Strategies

Tedarik Zinciri Yönetiminde Lojistik Optimizasyon Stratejileri

Types of Inventory

1- Raw Materials: These are the basic inputs required to produce your products. Think of wood for furniture makers or flour for bakeries.

2- Work-In-Progress (WIP): Items that are in the production process but aren't finished yet.

3- Finished Goods: Products ready to be sold to customers.

4- Maintenance, Repair, and Operations (MRO) Goods: Supplies used in the production process but aren't part of the final product.

Understanding these categories helps businesses manage their stock more effectively. I remember when we misclassified some of our WIP items as finished goods. It led to confusion and delayed shipments—a mistake we learned not to repeat!

The Hidden Costs of Excess Inventory

Holding excess inventory isn't just about physical space; it's like having money sitting on your shelves gathering dust. Here are some hidden costs:

Storage Costs: Warehousing isn't cheap. Rent, utilities, security, and maintenance add up quickly.

Insurance and Taxes: More inventory means higher insurance premiums and property taxes.

Obsolescence: Products can become outdated or expire, especially in tech and fashion industries.

Opportunity Costs: Capital tied up in inventory can't be used elsewhere—like investing in marketing or an online human resources management certificate program to boost your team's skills.

Benefits of Reducing Inventory

Reducing inventory comes with a slew of advantages:

Improved Cash Flow: Less money tied up means more liquidity for other investments.

Reduced Storage Costs: Smaller inventory requires less storage space, cutting down on overheads.

Investing in reducing inventory for profit maximization its a sure path to success.

Decreased Waste: Fewer products expire or become obsolete.

Enhanced Efficiency: Streamlined operations lead to faster response times and better customer service.

Higher Inventory Turnover Rate: Indicates efficient sales and restocking processes.

I can't emphasize enough how liberating it felt when we first decluttered our stockroom. Not only did we save on costs, but our team also became more productive without the chaos of excess stock.

Strategies for Reducing Inventory

Reducing inventory isn't about slashing stock recklessly. It's about strategic planning and smart management. Here are some tried-and-true strategies:

1. Just-In-Time (JIT) Management

Implementing JIT management means receiving goods only as they're needed in the production process. This reduces inventory costs significantly.

Benefits:

Minimizes storage needs.

Reduces waste from obsolete or expired products.

Increases efficiency in the production process.

Considerations:

Requires reliable suppliers.

Demands accurate demand forecasting.

During a trip to Japan, I visited a company that mastered JIT. Their efficiency was astounding—they had barely any storage space because they didn't need it! Everything arrived just in time, hence the name.

2. Improve Demand Forecasting

Accurate demand forecasting helps prevent overstocking and stockouts.

Methods:

Analyze historical sales data.

Monitor market trends.

Adjust for seasonal fluctuations.

When we started analyzing our sales patterns, we noticed spikes during certain seasons. Adjusting our orders accordingly prevented overstocking during slower periods.

3. Enhance Supply Chain Management

Efficient supply and chain management is crucial. By optimizing each step—from procurement to delivery—you can reduce lead times and inventory levels.

Actions:

Build strong relationships with suppliers.

Implement technology for better tracking.

Regularly review processes for improvements.

Consider enrolling in programs or workshops on SCM management to stay updated on best practices.

4. Utilize Inventory Management Software

Technology can be a game-changer. Modern software provides real-time data, automates ordering, and tracks inventory levels accurately.

Advantages:

Reduces human error.

Provides insights through data analytics.

Improves transparency across departments.

There's this story of a friend who runs a mid-sized manufacturing firm. After implementing inventory software, he saw a significant reduction in excess stock and could forecast demand more accurately.

5. Implement ABC Analysis

Categorize inventory based on importance:

1- A-Items: High-value, low-quantity items.

2- B-Items: Moderate value and quantity.

3- C-Items: Low-value, high-quantity items.

Focusing on 'A-Items' ensures you invest time and resources where it matters most.

6. Reduce Lead Time

Shortening the lead time—the period between ordering and receiving goods—helps lower inventory levels.

Strategies:

Source from local suppliers.

Improve internal procurement processes.

Use faster shipping methods.

By reducing our lead time, we could order stock more frequently in smaller quantities, keeping inventory levels optimal.

7. Conduct Regular Inventory Audits

Regular checks ensure that your inventory records match the physical stock.

Benefits:

Identifies discrepancies.

Prevents stockouts and overstocking.

Helps detect theft or loss.

Embracing Technology in Inventory Management

In today's digital age, leveraging technology is not just an option—it's a necessity.

Automation: Use of robotics and AI to manage stock levels.

IoT Devices: Sensors that provide real-time data on inventory status.

Data Analytics: Tools that analyze trends and predict future demand.

These technologies enhance supply chain management management by providing accurate data and reducing manual errors.

The Role of Human Resources

You might be wondering, what's HR got to do with inventory? Well, a lot! Training your staff on inventory management best practices is essential.

Staff Training: Investing in courses or an online human resources management certificate program can equip your team with the necessary skills.

Employee Engagement: Motivated employees are more likely to adhere to processes and suggest improvements.

Cross-Functional Teams: Encouraging collaboration between departments enhances overall efficiency.

Personal Anecdote: Lessons Learned

I'll never forget when we had a major mishap due to poor inventory management. We had just launched a new product line, and excitement was high. However, we underestimated the demand and ended up with significant stockouts. Customers were frustrated, and we lost potential sales.

That experience was a wake-up call. We realized the importance of not only reducing excess inventory but also ensuring that we met customer demand. It led us to overhaul our entire approach, incorporating many of the strategies I've mentioned.

Bullet Points for Quick Reference

Benefits of Reducing Inventory:

Cost savings

Improved cash flow

Enhanced efficiency

Better customer satisfaction

Strategies to Implement:

Just-In-Time management

Improve demand forecasting

Enhance supply chain processes

Utilize inventory management software

Conduct regular audits

Common Mistakes to Avoid

1- Neglecting Data Analysis

Ignoring sales trends can lead to overstocking or stockouts.

2. Over-reliance on Suppliers

Without backup suppliers, you risk delays if one can't deliver.

3. Failing to Train Staff

Uninformed employees may not follow protocols diligently.

4. Ignoring Technology

Manual processes are prone to errors and inefficiencies.

Conclusion

Reducing inventory is more than just a cost-saving measure; it's a strategic approach to streamline operations and boost profitability. By adopting methods like JIT management and enhancing management chain supply, businesses can respond swiftly to market changes, reduce waste, and improve customer satisfaction.

Reflecting on my own journey, I can attest that the effort to optimize inventory pays off manifold. Not only did we see financial benefits, but our operations became smoother, and our team was more aligned with our goals.

Remember, it's not about having the least amount of stock possible; it's about having the right amount at the right time. With careful planning, embracing technology, and investing in your team's skills, you can master inventory management.

Investing in reducing inventory for profit maximization—it's a sure path to success.

References

Ballou, R. H. (2004). Business Logistics/Supply Chain Management (5th ed.). Pearson Education.

Krajewski, L. J., Ritzman, L. P., & Malhotra, M. K. (2013). Operations Management: Processes and Supply Chains (10th ed.). Pearson.

Monczka, R. M., Handfield, R. B., Giunipero, L. C., & Patterson, J. L. (2015). Purchasing and Supply Chain Management (6th ed.). Cengage Learning.

Murthy, D. N. P., & Blischke, W. R. (2006). Warranty Management and Product Manufacture. Springer Science & Business Media.

Stevenson, W. J. (2018). Operations Management (13th ed.). McGraw-Hill Education.

Frequently Asked Questions

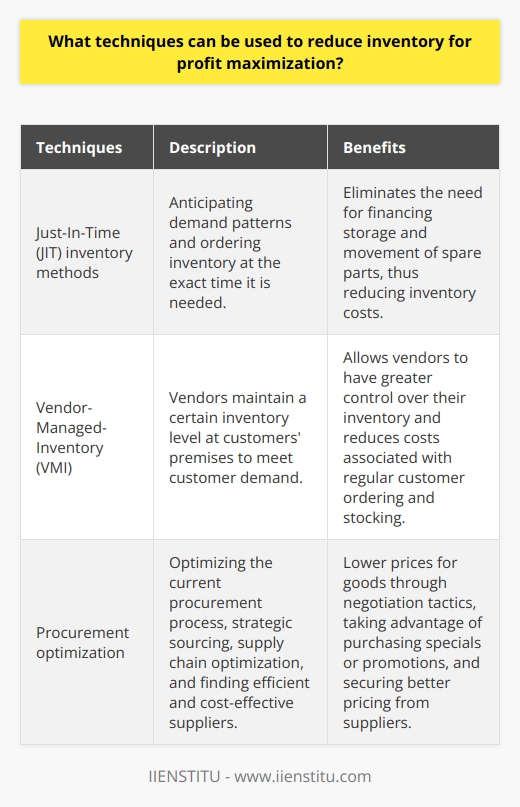

What techniques can be used to reduce inventory for profit maximization?

Inventory management is one of the critical components of managing a successful business. Without proper management, a company can tie up much of its cash flow in holding too much stock and incur additional costs in obsolescence. By reducing their inventory, companies can often significantly increase their profit margins. Here we look at some techniques that can be used to reduce inventory for profit maximization.

The first technique is to use Just-In-Time (JIT) inventory methods. JIT is a technique that involves anticipating demand patterns and ordering inventory at the exact time it is needed. This reduces inventory costs, as businesses no longer need to finance the storage and movement of spare parts. Companies can take advantage of JIT by analyzing customers’ demands and forecasting future needs. Technology such as enterprise resource planning (ERP) systems can be utilized to track customer orders and suggest purchases accordingly.

The second technique is to utilize the concept of Vendor-Managed-Inventory (VMI). VMI involves the vendor maintaining a certain inventory level at a customer’s premises to meet customer demand. This allows the vendor to maintain more immediate control over their list, reducing costs as they no longer have to pay for regular customer ordering and stocking costs. By using predictive analytics, companies can accurately forecast customer demand and ensure they always keep the proper inventory levels.

The third technique is to optimize their current procurement process. Companies can focus on strategic sourcing, optimizing their supply chain, and finding the most efficient, cost-effective suppliers. They can also utilize negotiation tactics to obtain lower prices for the goods they purchase. Additionally, companies can take advantage of purchasing specials, promotions, or group buying to get better pricing from their suppliers.

Reducing inventory for profits is achievable when the proper fundamental techniques and tools are used. With careful analysis and implementation of JIT, VMI, and procurement optimization, businesses can increase their profits with reduced inventory costs.

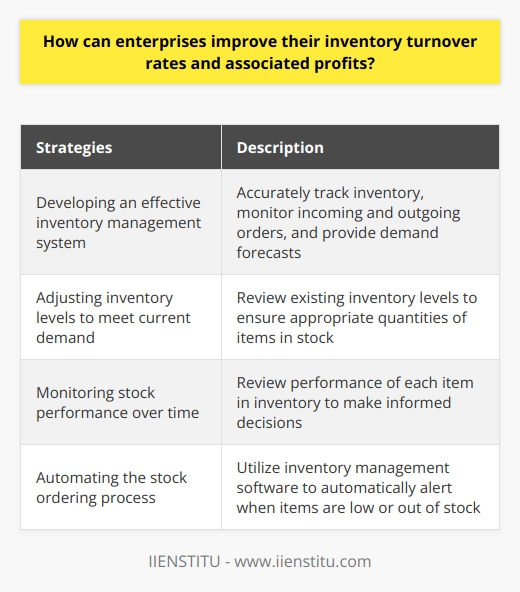

How can enterprises improve their inventory turnover rates and associated profits?

In modern businesses, inventory turnover rate and associated profits greatly influence the success of an enterprise. Therefore, keeping a steady inventory flow throughout the organization and optimizing its stock value is integral to any business’s overall health. In this article, we will propose some tips and strategies that enterprises can apply to improve their inventory turnover rate to maximize profits.

The first and most important tip is to develop an effective inventory management system. This system should accurately record what is on hand, what is being ordered or used, and what remains in stock. This system should also be able to track all incoming and outgoing orders, allowing for the automatic restocking of necessary items when necessary. Additionally, it should be able to provide forecasts of expected demand for the next few months, allowing for the identification of essential supply issues.

Second, enterprises should adjust their inventory levels to meet the current demand. Not having enough inventory on hand can cause delays in order fulfillment, while excessive inventory can result in losses due to a lack of sales. Therefore, enterprises should review their current inventory levels to ensure they have the right quantities of items in stock.

Third, enterprises should track their stock performance over time. Reviewing the version of each item in the inventory helps businesses identify which items are the most profitable and which need improvement. This allows the enterprise to make informed decisions regarding what to keep in stock and what to discontinue.

Finally, enterprises should consider automatizing the stock ordering process. For example, modern inventory management software solutions can automatically alert the warehouse when an item runs out or is low on stock, thus enabling enterprises to respond quickly to sudden demand changes and improve their order fulfillment processes.

In conclusion, effective inventory management systems, dynamic stock levels, stock performance monitoring, and automated stock ordering are just a few strategies enterprises can use to improve their inventory turnover rates and maximize profits. With the right combination of these measures, enterprises can ensure that they remain competitive in their market while still meeting the demands of their customers.

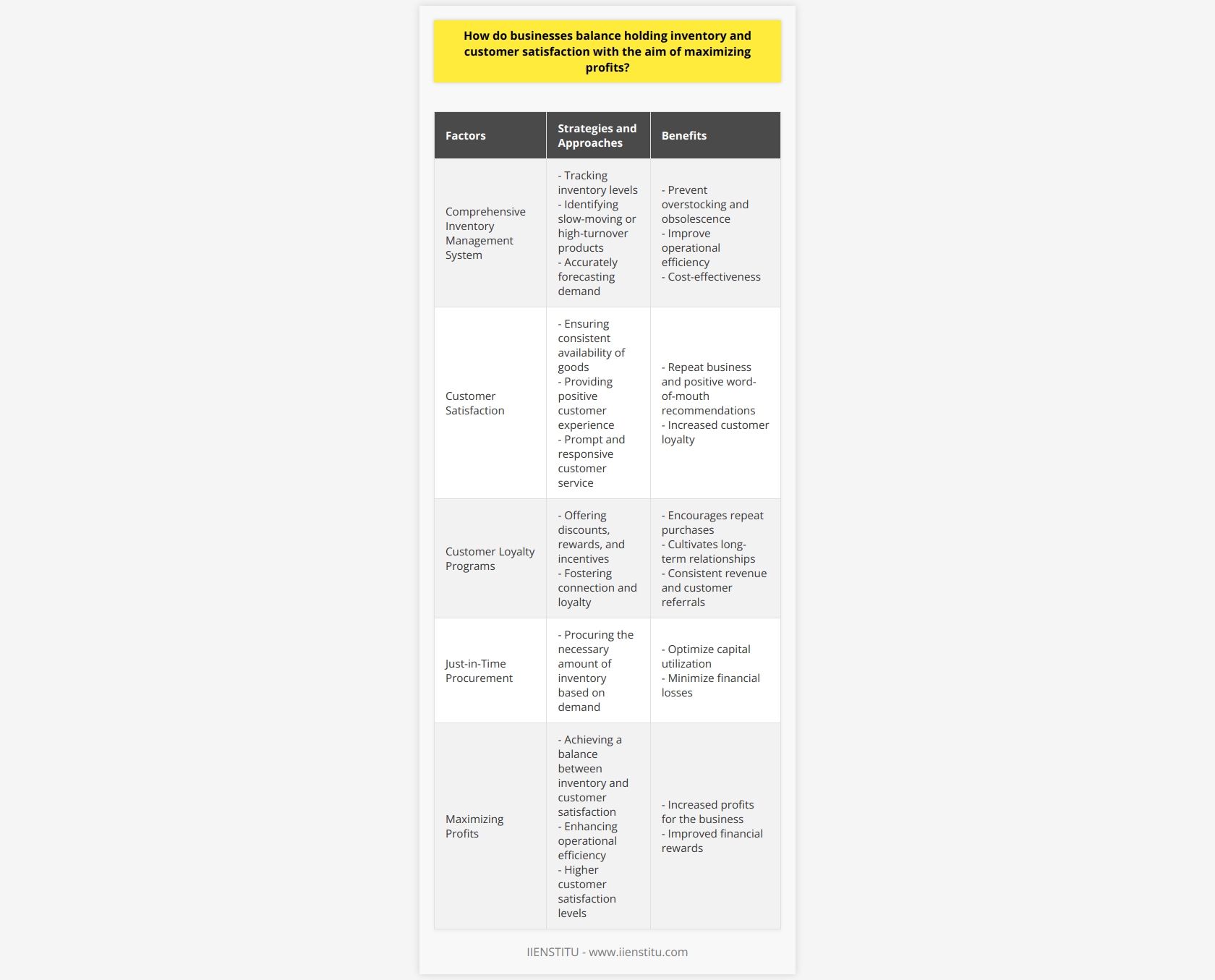

How do businesses balance holding inventory and customer satisfaction with the aim of maximizing profits?

In the ever-evolving business world, inventory management and customer service are essential components to maximizing profits. An effective balance between these areas of operation can provide a strong foundation for a successful business. This article will discuss how companies can balance inventory and customer satisfaction to maximize profits.

One key factor to consider is developing a comprehensive inventory management system. Such a system should include tracking inventory levels, identifying slow-moving or high-turnover items, and forecasting demand. This will ensure that the right amount of inventory is procured to meet customer demand while preventing overstocking and obsolescence. Another inventory-related factor is the implementation of just-in-time (JIT) procurement processes that allow businesses to minimize the costs associated with storing and handling goods.

Aside from inventory management, businesses must also strive to ensure customer satisfaction. To do this, they must ensure that goods are available when promised and that the customer experience is positive. This can be achieved through attentive customer service and effective order execution. Businesses should also seek to create customer loyalty programs, such as discounts and rewards, to foster a sense of connection with customers.

To maximize profits, businesses must strike a solid balance between inventory and customer satisfaction. Developing a comprehensive inventory management system, implementing JIT processes, and creating customer loyalty programs can help to achieve this balance. By doing so, businesses can benefit from a more efficient and cost-effective operating model and greater customer satisfaction, ultimately leading to more profits.

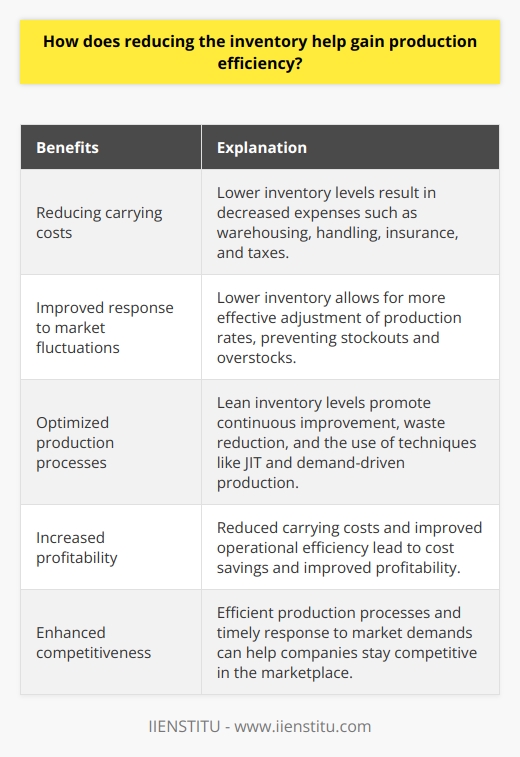

How does reducing the inventory help gain production efficiency?

Enhancing Production Efficiency through Inventory Reduction

Reducing inventory in a production process can lead to significant increases in operational efficiency, resulting in cost savings and improved profitability. This can happen through several channels, including the reduction of carrying costs, improved response to market fluctuations, and the optimization of production processes.

Reduced Carrying Costs

One of the primary benefits of reducing inventory is the decrease in carrying costs associated with holding, storing, and managing excess stock. These costs can include expenses such as warehousing, handling, insurance, and taxes. By maintaining lower inventory levels, a business can allocate resources more effectively and lower their overall operating expenses.

Improved Response to Market Fluctuations

A second advantage of inventory reduction is the ability to respond more quickly to changes in market demand. When a company maintains lower inventory levels, it can adjust production rates more effectively as market conditions change. This flexibility can prevent stockouts, overstock situations, and potential losses, leading to higher customer satisfaction and increased sales.

Optimized Production Processes

Lastly, reducing inventory can lead to more efficient production processes. When a company focuses on maintaining lean inventory levels, it encourages continuous improvement and waste reduction in every aspect of the operation. The use of tools such as just-in-time (JIT) and demand-driven production techniques can help businesses eliminate bottlenecks, streamline workflows, and maximize the value of their resources.

In conclusion, reducing inventory can benefit a company's production efficiency in various ways, including the reduction of carrying costs, enhanced response to market fluctuations, and the optimization of production processes. By implementing inventory reduction strategies, businesses can improve their overall profitability and competitiveness in the marketplace.

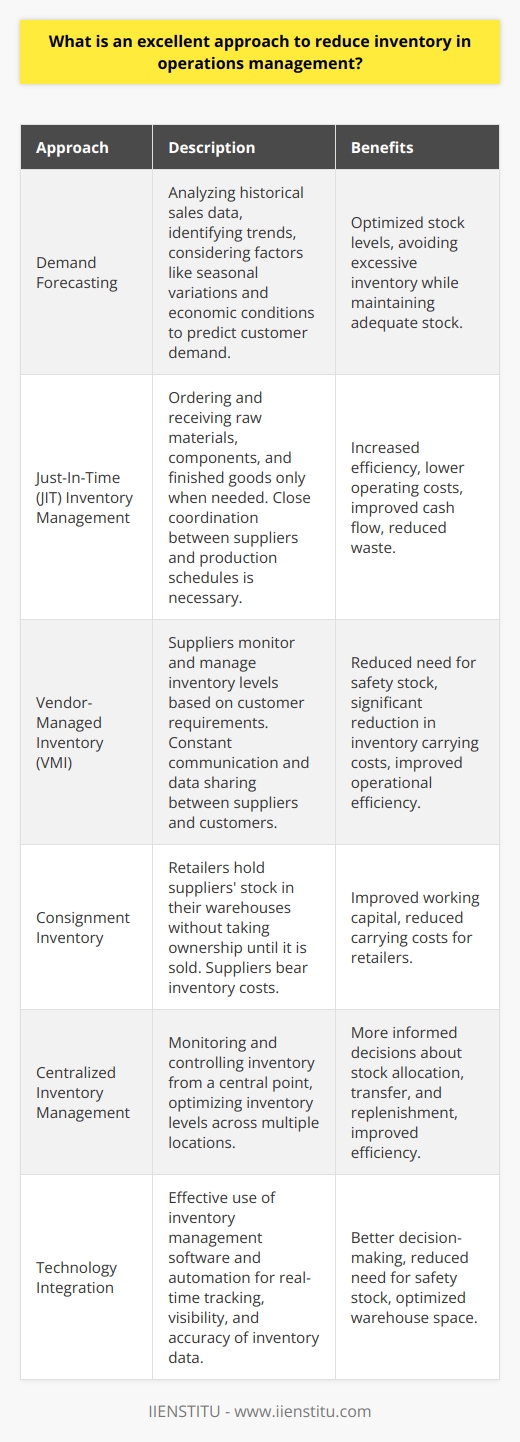

What is an excellent approach to reduce inventory in operations management?

Approach to Reduce Inventory

**Demand Forecasting**

Accurate demand forecasting is crucial for reducing inventory levels. By closely analyzing historical sales data, identifying trends, and considering factors such as seasonal variations and economic conditions, managers can better predict customer demand. This allows them to make informed decisions about stock levels, enabling them to avoid excessive inventory while maintaining adequate stock to fulfill customer needs.

**Just-In-Time (JIT) Inventory Management**

The JIT approach focuses on minimizing inventory by ordering and receiving raw materials, components, and finished goods only when needed. This requires close coordination between suppliers and production schedules, ensuring timely delivery of inputs to prevent stockouts or delays. By reducing inventory levels and minimizing waste, JIT can lead to increased efficiency, lower operating costs, and improved cash flow.

**Vendor-Managed Inventory (VMI)**

In VMI arrangements, suppliers monitor and manage inventory levels based on customer requirements. Through constant communication and data sharing, they ensure that stock levels are maintained according to agreed-upon service levels, reducing the need for safety stock. This can lead to a significant reduction in inventory carrying costs and improve overall operational efficiency.

**Consignment Inventory**

Implementing a consignment inventory approach allows retailers to hold suppliers' stock in their warehouses without taking ownership until it is sold. With suppliers bearing the responsibility for inventory costs, retailers can focus on reducing on-hand inventory, improving working capital and reducing carrying costs.

**Centralized Inventory Management**

With centralized inventory management, companies can optimize inventory levels across multiple locations. By monitoring and controlling inventory from a central point, companies can make more informed decisions about stock allocation, transfer, and replenishment, leading to reduced inventory levels and improved overall efficiency.

**Effective Use of Technology**

Integration of technology, such as inventory management software and automation, can significantly improve inventory tracking, visibility, and accuracy. Accurate real-time inventory data enables better decision-making and forecasting, reducing the need for safety stock and optimizing available warehouse space.

In conclusion, by adopting strategies such as demand forecasting, JIT inventory management, VMI, consignment inventory, centralized inventory management, and the effective use of technology, companies can significantly reduce inventory levels. These approaches lead to increased operational efficiency, lower costs, and improved overall profitability.

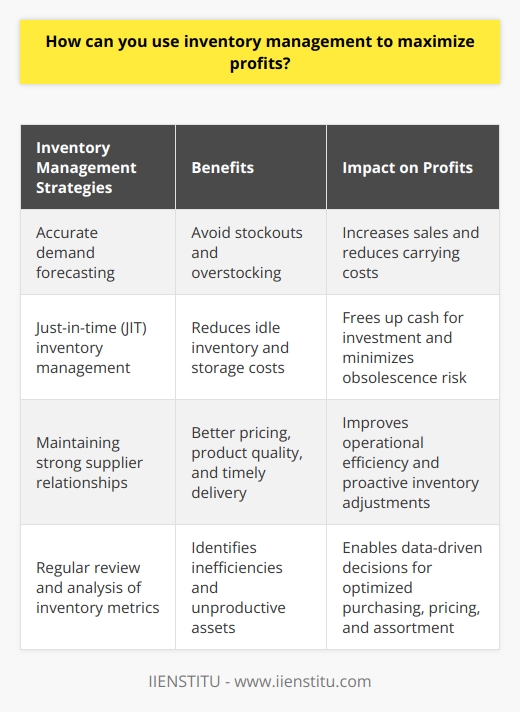

How can you use inventory management to maximize profits?

Effective Inventory Management Strategies

Using inventory management to maximize profits involves implementing effective strategies that maintain an optimal level of inventory while minimizing costs associated with overstocking, stockouts, and obsolescence. Proper inventory management ensures that businesses have the right products, in the right quantities, at the right time to meet customer demands and maximize sales.

Demand Forecasting and Inventory Optimization

Accurate demand forecasting is crucial for determining the optimal level of inventory needed to satisfy customer demand. By analyzing historical sales data, seasonal trends, and market conditions, businesses can anticipate fluctuations in demand and adjust their inventory accordingly. This helps in avoiding stockouts, which can lead to lost sales and unsatisfied customers, as well as overstocking, which ties up working capital and increases carrying costs.

Just-In-Time Inventory Management

A just-in-time (JIT) inventory management approach can help businesses maximize profits by minimizing inventory carrying costs. JIT entails ordering and receiving inventory only when it is needed for production or sales, thus reducing the amount of idle inventory sitting on the shelves. This approach reduces storage and insurance costs, minimizes the risk of inventory obsolescence, and frees up cash for investment in other areas of the business.

Vendor Management and Supplier Relationships

Maintaining strong relationships with suppliers can significantly impact inventory management and overall profitability. By establishing collaborative partnerships with suppliers, businesses can negotiate better pricing, improve product quality, and ensure timely delivery of inventory. Moreover, vendors can provide valuable insights into market trends and emerging customer needs, allowing businesses to be more proactive in adjusting their inventory levels.

Inventory Turnover and Performance Metrics

Regularly reviewing and analyzing inventory turnover and other key performance metrics helps businesses uncover inefficiencies in their inventory management processes. Higher inventory turnover indicates that a business is effectively utilizing its inventory to generate sales, while slow-moving inventory may indicate unproductive assets or weak demand for certain products. Tracking these metrics allows businesses to make data-driven decisions about purchasing, pricing, and product assortment to maximize profits.

In conclusion, implementing effective inventory management strategies can help businesses maximize profits by efficiently meeting customer demand, reducing inventory-related costs, and improving overall operational efficiency. By focusing on demand forecasting, just-in-time inventory management, vendor relationships, and performance metrics analysis, businesses can optimize their inventory levels and drive sustainable growth.